Sign in for Premium Content

If you are a client, sign in below to access premium content.

Stocks rebounded during the holiday-shortened week as gains in overseas stock markets spurred buying activity, giving the Dow its best week since March. Despite the buying pressure, investors curbed their enthusiasm ahead of the Federal Reserve meeting next week. For the week, the S&P 500 gained 2.07%, the Dow grew 2.05%, and the NASDAQ gained 2.96%.1

I mentioned last week on RTL Europe (Europe’s largest TV network), that the market will be going through a ‘bottoming process’ for some time. As much as we would like the Dow to recover back to 18,000 quickly, a lot of ‘technical damage has been done.

I also mentioned to the network, that China is slowing down; it is also a proxy for world demand. Since 2010, China has been the largest manufacturer in the world (ousting the US). It is why that when China ‘sneezes’, the rest of the world catches a cold.

China’s Growth Sputters

Fresh data out of China showed that factory output missed expectations, supporting the view that China’s economic growth may dip below 7% for the first time since the global recession. Infrastructure investment also fell, leading many experts to believe that China’s central government may be forced to roll out new measures to boost economic growth.2

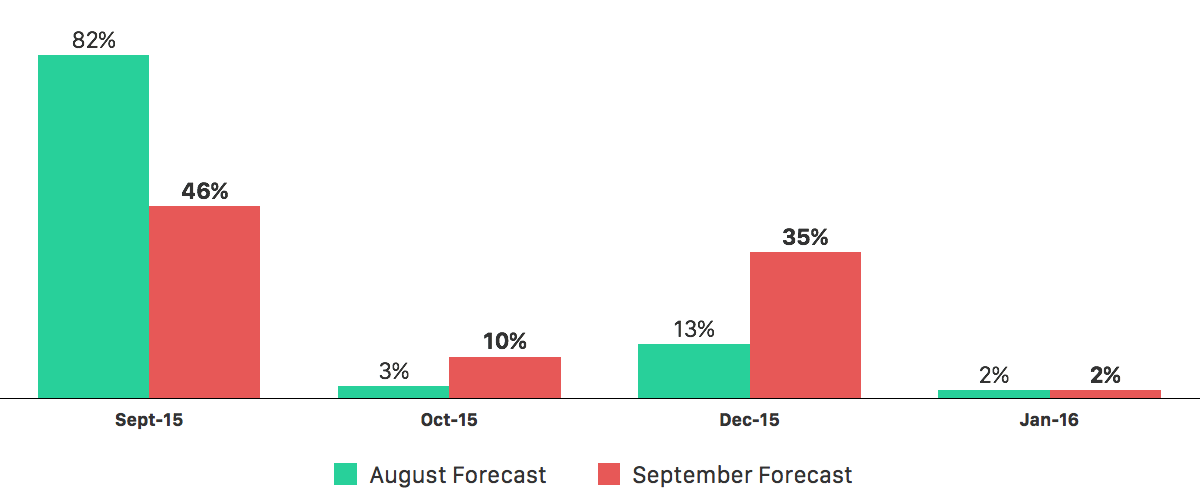

All Eyes on the Fed

This week, the eyes of the world will be on the Federal Reserve as the Open Market Committee votes on whether to raise interest rates for the first time in nearly a decade. The FOMC meets Wednesday and Thursday and will issue their official statement Thursday afternoon. The most recent Wall Street Journal survey of private economists shows that experts are split. Last month, a whopping 82% of economists thought that the Fed would pull the trigger this week; now, just 46% think the Fed will act this month.3

Wall Street Journal Survey of Economists

{ Source: Wall Street Journal Economic Forecasting Survey. August & September 2015 Editions }

There are strong arguments to make on both sides of the issues. On the pro-rate-hike side are the opinions that too much easy money may fuel asset bubbles. Near-zero-rates also leave the Fed without ammunition in the event of another downturn.

On the hold-rates-steady side is the opinion that recent market volatility and ongoing concerns about global economic growth could spark another spate of selling if the Fed moves to raise rates now.4

Realistically, if the Fed moves this week to raise rates, they will likely announce a quarter-point raise to target interest rates in the 0.25%-0.50% range. How will markets react to a rate decision? It’s hard to say. Investors might view an increase as a vote of confidence in the economy and rally. Alternately, sentiment might sour on fears of a new economic downturn. As always, we’re keeping an eye on the situation and will update you as necessary.

INVESTING RISK DISCLOSURE

Keep in mind that investing involves risk. The value of your investment will fluctuate over time and you may gain or lose money. Before investing, consider the funds’ investment objectives, risks, charges, and expenses. Contact Mahoney Asset Management for a prospectus or, if available, a summary prospectus containing this information. Read it carefully.

IMPORTANT CONSUMER INFORMATION

This web site has been prepared solely for informational purposes. It is not an offer to buy or sell any security; nor is it a solicitation of an offer to buy or sell any security.This site and the opinions and information therein are based on sources which we believe to be dependable, but we can not guarantee the accuracy of such information.

Representatives of a broker-dealer or investment adviser may only conduct business in a state if the representatives and the broker-dealer or investment adviser they represent: (a) satisfy the qualification requirements of, and are approved to do business by, the state; or (b) are excluded or exempted from the state’s licenser requirements.

An investor may obtain information concerning a broker-dealer, an investment advisor, or a representative of a broker-dealer or an investment advisor, including their licenser status and disciplinary history, by contacting the investor’s state securities law administrator.

The financial calculator results shown represent analysis and estimates based on the assumptions you have provided, but they do not reflect all relevant elements of your personal situation. The actual effects of your financial decisions may vary significantly from these estimates–so these estimates should not be regarded as predictions, advice, or recommendations. Mahoney Asset Managment does not provide legal or tax advice. Be sure to consult with your own tax and legal advisors before taking any action that would have tax consequences.

SECURITIES: ARE NOT FDIC-INSURED/ARE NOT BANK-GUARANTEED/MAY LOSE VALUE

This information is intended for use only by residents of CA, CT, DC, FL,, MA, MD, MN, NC, NJ, NY, OH, PA, and VA. Ken Mahoney may only conduct securities business with residents of the states and/or jurisdiction for which they are properly registered.

Securities offered through Newbridge Securities Corporation, member FINRA, SIPC.

Investment Advisory services through NFSG Corporation an SEC Registered Investment Advisor.

Office of Supervisory Jurisdiction: 1200 N. Federal Hwy., Ste. 400, Boca Raton, FL 33432. Phone 954.334.3450 Fax 954.489.2390

Specific recommendations can only be based on review of a number of suitability factors including but not limited to the investors financial profile, investment objectives, risk tolerance and the investors review of appropriate offering documents. Past performance is no guarantee of future results. To help you make informed decisions, we provide you with essential disclosures, such as Regulation Best Interest (Reg BI), the Client Relationship Summary (CRS), and Form ADV. Linked sites are strictly provided as a courtesy. Newbridge Securities, Inc. does not guarantee, approve nor endorse the information or products available at the sites, nor do links indicate any association with or endorsement of the linked sites by Newbridge Securities.