Sell in May and go away is a well-known trading adage that warns investors to sell their stock holdings in May to avoid a seasonal decline in equity markets. The “sell in May and go away” strategy is that an investor who sells his or her stock holdings in May and gets back into the equity market in November – thereby avoiding the typically volatile May-October period – would be much better off than an investor who stays in equities throughout the year. While past history shows that markets perform better Oct through April, its very difficult for investors to try use seasonality as their only decision making process.

If you are a client, sign in below to access exclusive content.

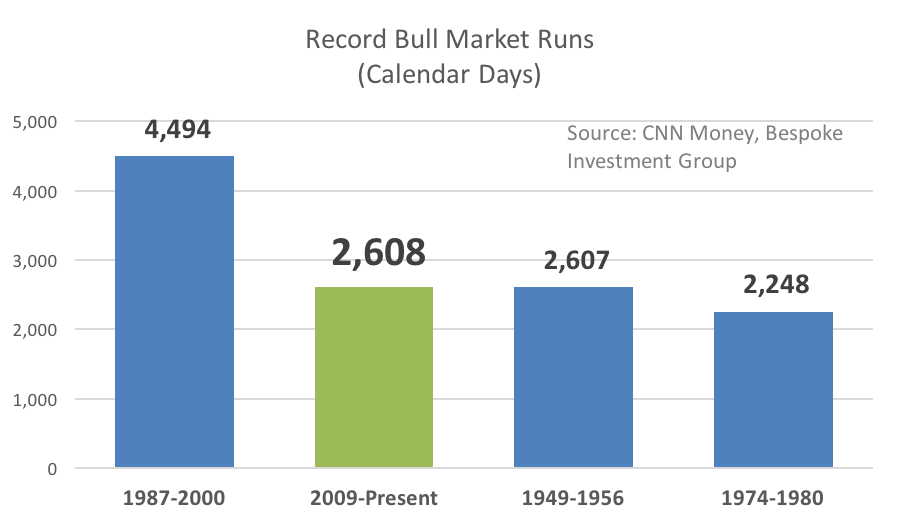

As of Friday, the S&P 500 is on the second-longest bull market run in history, surpassing the 1949-1956 bull market that lasted 2,607 days. The longest bull market in history ran between 1987 and 2000, lasting nearly 4,500 days.1

After months of volatility and challenges on the horizon, can the bulls keep running?

In the pro-bull column, we have a few major points to consider

Bull markets don’t just die of old age. History shows us that bull markets ended because of a variety of shocks like oil price spikes, recessions, bursting asset bubbles, geopolitical issues, and extreme leveraging.2 While the past doesn’t predict the future, we should evaluate threats to market performance instead of worrying about birthdays.

Economic indicators support growth. Recessions have accompanied or presaged many previous bear markets. Currently, economic indicators like a growing job market, low gas prices, and a healthy housing market point to sustainable—though moderate—economic growth. Even when recession risks are higher this year, most economists don’t see an economic downturn in the short-term future.3

We have experienced healthy pullbacks. One of the markers of a bull market top is elevated investor optimism and unsustainably high stock valuations. Since the last S&P 500 market high in May of 2015, markets have retrenched several times as investors have taken stock of global risks to growth. We haven’t seen the irrational exuberance that often foreshadows a bear market turn.

In the pro-bear column, we also have some points to weigh in our thinking

Threats to economic growth from China and Europe may prove too much for markets. We don’t know that we have seen the worst out of China, and a hard landing of the world’s second-largest economy would send ripples throughout the global economy that could threaten markets. Europe is grappling with political, economic, and security issues that could threaten the EU.

The Federal Reserve may bungle monetary policy. The Fed is performing a very delicate dance to bring interest rates closer to historic levels. Raise rates too fast and the economy could stumble; raise them too slowly and the Fed could leave itself unable to fight off another economic slowdown. A monetary policy misstep could trigger a market downturn.

Corporate profits may continue to fall. U.S. companies are struggling to find growth amid challenging global conditions; earnings declined year-over-year for the fifth quarter in a row last quarter, and continued weakness could cause investors to become bearish about U.S. stocks.4

Our view

The simple truth is that no one can predict market tops or bottoms; plenty of people say they can, but it’s all a matter of educated (or uneducated) guesswork. Instead of trying to call markets, what we do is take a look at overall domestic and international fundamentals and create portfolio strategies that align with our clients’ overall goals. We can assume that the current bull market will come to an end someday; to reach the #1 spot it would have to continue through 2021, and that’s a pretty big stretch.5 Rather than worrying about when the end might come, we’ll adjust portfolio strategies as needed and prudently position our clients for risk.

If you have any questions about market strategies for volatile times, please give us a call.

Sources

INVESTING RISK DISCLOSURE

Keep in mind that investing involves risk. The value of your investment will fluctuate over time and you may gain or lose money. Before investing, consider the funds’ investment objectives, risks, charges, and expenses. Contact Mahoney Asset Management for a prospectus or, if available, a summary prospectus containing this information. Read it carefully.

IMPORTANT CONSUMER INFORMATION

This web site has been prepared solely for informational purposes. It is not an offer to buy or sell any security; nor is it a solicitation of an offer to buy or sell any security.This site and the opinions and information therein are based on sources which we believe to be dependable, but we can not guarantee the accuracy of such information.

Representatives of a broker-dealer or investment adviser may only conduct business in a state if the representatives and the broker-dealer or investment adviser they represent: (a) satisfy the qualification requirements of, and are approved to do business by, the state; or (b) are excluded or exempted from the state’s licenser requirements.

An investor may obtain information concerning a broker-dealer, an investment advisor, or a representative of a broker-dealer or an investment advisor, including their licenser status and disciplinary history, by contacting the investor’s state securities law administrator.

The financial calculator results shown represent analysis and estimates based on the assumptions you have provided, but they do not reflect all relevant elements of your personal situation. The actual effects of your financial decisions may vary significantly from these estimates–so these estimates should not be regarded as predictions, advice, or recommendations. Mahoney Asset Managment does not provide legal or tax advice. Be sure to consult with your own tax and legal advisors before taking any action that would have tax consequences.

SECURITIES: ARE NOT FDIC-INSURED/ARE NOT BANK-GUARANTEED/MAY LOSE VALUE

This information is intended for use only by residents of CA, CT, DC, FL,, MA, MD, MN, NC, NJ, NY, OH, PA, and VA. Ken Mahoney may only conduct securities business with residents of the states and/or jurisdiction for which they are properly registered.

Securities offered through Newbridge Securities Corporation, member FINRA, SIPC.

Investment Advisory services through NFSG Corporation an SEC Registered Investment Advisor.

Office of Supervisory Jurisdiction: 1200 N. Federal Hwy., Ste. 400, Boca Raton, FL 33432. Phone 954.334.3450 Fax 954.489.2390

Specific recommendations can only be based on review of a number of suitability factors including but not limited to the investors financial profile, investment objectives, risk tolerance and the investors review of appropriate offering documents. Past performance is no guarantee of future results. To help you make informed decisions, we provide you with essential disclosures, such as Regulation Best Interest (Reg BI), the Client Relationship Summary (CRS), and Form ADV. Linked sites are strictly provided as a courtesy. Newbridge Securities, Inc. does not guarantee, approve nor endorse the information or products available at the sites, nor do links indicate any association with or endorsement of the linked sites by Newbridge Securities.