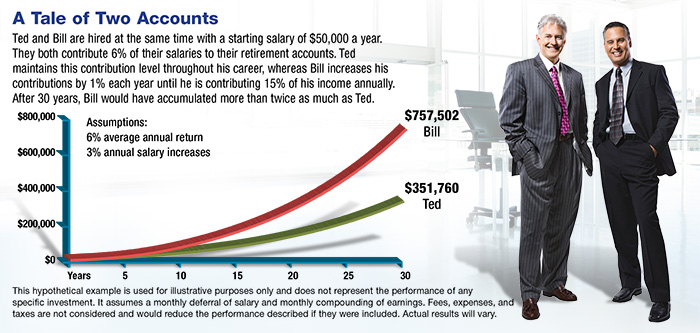

In a survey of workers who participate in an employer-sponsored retirement plan, 71% said they wanted their employers to increase their savings rate automatically by 1% each year.1 Some plans have auto-escalation features that increase workers’ contributions by a percentage point on an annual basis.2 Regardless of whether you save by default or by choice, increasing your retirement contributions could make a big difference in the amount you accumulate during your working years (see chart).

Although there’s nothing magical about a 1% annual increase, it may be a manageable way to get closer to an appropriate contribution level for your age and personal situation. Industry estimates suggest that workers need to save 13% to 15% of salary throughout their careers in order to fund a retirement lifestyle equivalent to their pre-retirement standards of living.3 People who don’t start saving until later in life may have to save a higher percentage.

Here are a few suggestions that could help you save more without making major changes to your current lifestyle.

Save your raise

When you receive a raise, it’s tempting to increase your spending, but it’s also a great opportunity to increase your retirement savings. Even if you need some of the additional income for current expenses, you could divert a portion of it to your retirement account. And when you contribute on a pre-tax basis, the difference in your take-home pay may not be as significant as you might expect.

Make payments to your future

If you pay off the balance on a car loan, student loan, or credit card, you could continue making the same monthly payments directly to your retirement account. Because the payment is already part of your monthly budget, this provides a way to help increase your savings without a major change to your cash flow.

Pay as you go

Paying off a credit card may allow you to save more, but it might be wiser to avoid credit-card debt in the first place. Unless you pay off your balance in full each month, credit-card interest can grow quickly and could stand in the way of building the retirement savings you may need.

Limit the daily treats

You deserve an occasional treat, but spending on “little things” can add up over time. For example, if you stop for a $3.50 latte each day on your way to work and have another one in the afternoon, you would spend about $150 each month. If this amount was instead invested in an account earning a 6% annual return, you could accumulate more than $100,000 after 25 years.

This hypothetical example is used for illustrative purposes only and does not represent the performance of any specific investment. Fees, expenses, and taxes are not considered and would reduce the performance described if they were included. Actual results will vary.

Saving for retirement may seem daunting, but small steps could make a big difference for your financial future.

1) AdvisorOne.com, January 17, 2013

2) Defined Contribution Institutional Investment Association, 2013

3) Employee Benefit News, May 7, 2013

INVESTING RISK DISCLOSURE

Keep in mind that investing involves risk. The value of your investment will fluctuate over time and you may gain or lose money. Before investing, consider the funds’ investment objectives, risks, charges, and expenses. Contact Mahoney Asset Management for a prospectus or, if available, a summary prospectus containing this information. Read it carefully.

IMPORTANT CONSUMER INFORMATION

This web site has been prepared solely for informational purposes. It is not an offer to buy or sell any security; nor is it a solicitation of an offer to buy or sell any security.This site and the opinions and information therein are based on sources which we believe to be dependable, but we can not guarantee the accuracy of such information.

Representatives of a broker-dealer or investment adviser may only conduct business in a state if the representatives and the broker-dealer or investment adviser they represent: (a) satisfy the qualification requirements of, and are approved to do business by, the state; or (b) are excluded or exempted from the state’s licenser requirements.

An investor may obtain information concerning a broker-dealer, an investment advisor, or a representative of a broker-dealer or an investment advisor, including their licenser status and disciplinary history, by contacting the investor’s state securities law administrator.

The financial calculator results shown represent analysis and estimates based on the assumptions you have provided, but they do not reflect all relevant elements of your personal situation. The actual effects of your financial decisions may vary significantly from these estimates–so these estimates should not be regarded as predictions, advice, or recommendations. Mahoney Asset Managment does not provide legal or tax advice. Be sure to consult with your own tax and legal advisors before taking any action that would have tax consequences.

SECURITIES: ARE NOT FDIC-INSURED/ARE NOT BANK-GUARANTEED/MAY LOSE VALUE

This information is intended for use only by residents of CA, CT, DC, FL,, MA, MD, MN, NC, NJ, NY, OH, PA, and VA. Ken Mahoney may only conduct securities business with residents of the states and/or jurisdiction for which they are properly registered.

Securities offered through Newbridge Securities Corporation, member FINRA, SIPC.

Investment Advisory services through NFSG Corporation an SEC Registered Investment Advisor.

Office of Supervisory Jurisdiction: 1200 N. Federal Hwy., Ste. 400, Boca Raton, FL 33432. Phone 954.334.3450 Fax 954.489.2390

Specific recommendations can only be based on review of a number of suitability factors including but not limited to the investors financial profile, investment objectives, risk tolerance and the investors review of appropriate offering documents. Past performance is no guarantee of future results. To help you make informed decisions, we provide you with essential disclosures, such as Regulation Best Interest (Reg BI), the Client Relationship Summary (CRS), and Form ADV. Linked sites are strictly provided as a courtesy. Newbridge Securities, Inc. does not guarantee, approve nor endorse the information or products available at the sites, nor do links indicate any association with or endorsement of the linked sites by Newbridge Securities.