Many Americans are familiar with Social Security’s projected shortfall and the public debate on how to fix the program’s finances. Going forward, fewer workers will support a larger number of retiring baby boomers. Without some combination of tax increases and benefit cuts, Social Security’s operating deficit is expected to exceed $800 billion over the next 10 years.¹

Some of the nation’s public- and private-sector pension plans are facing similar financial challenges. Unlike defined-contribution plans such as 401(k)s, pensions are defined-benefit plans that promise to pay lifetime benefits to retirees based on length of service and their pre-retirement salaries.

Pension plans that become severely underfunded could eventually fail, leaving participants without the retirement incomes they were counting on, or transferring the burden to taxpayers if a government bailout is needed.

Here’s a closer look at how pensions operate and why more of these retirement plans may be under pressure.

Dealing with Deficits

Investment losses from the 2008 financial crisis reduced public pension assets, and some states chose not to make their full recommended contributions.² An estimated $800 billion in unfunded liabilities for public-employee pensions has been reported, with individual state funding levels ranging widely from 40% to 80%.³

A long period of low interest rates has taken a toll on private-sector pensions. The funding deficit of the 100 biggest corporate pension plans rose to $411.8 billion at the end of 2012, and the plans were 76.4% funded (on average). A funding ratio of 80% is usually considered healthy.4

Low rates affect the calculation of a plan’s funding ratio by increasing the value of future benefit obligations (or liabilities). Such liability losses have more than offset investment gains that exceeded expectations in three of the last four years.5 For individual companies, a loss of funding status typically results in a charge to their balance sheets at the end of the fiscal year and increases pension expenses the following year.

Repercussions for Retirees

To help reduce pension costs, 45 states have cut benefits for teachers, police, firefighters, and other public workers. Because most major changes affect only new workers, much of the savings won’t be realized for several decades. Twelve states, however, have reduced benefits for current retirees, including nine that suspended cost-of-living increases.6

To help control costs, some corporations are closing pensions to new employees, freezing benefits for current workers, or terminating plans and offering lump-sum payments. Many companies are switching to defined-contribution plans in which the workers bear the investment risks.7

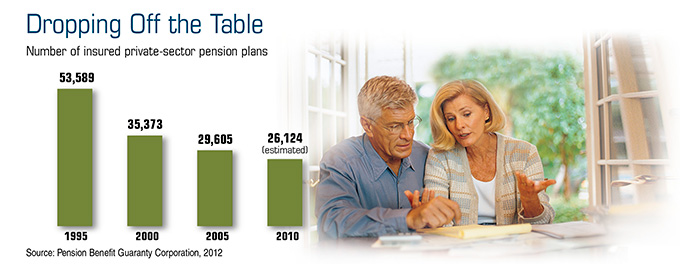

The Pension Benefit Guaranty Corporation (PBGC) is a U.S. government agency that provides basic pension benefits for participants of failed private-sector plans. The PBGC is funded by insurance premiums and recovered assets, not tax dollars, but is itself operating under a growing deficit in recent years.

Because most private-sector (and some public-sector) pension benefits do not rise with inflation, a fixed benefit amount that seems adequate initially might cover a much smaller share of a retiree’s living expenses after 20 years.

Public and private pensions are operating in a difficult environment, and some plan sponsors may not be able to keep all the promises that were made to workers. Therefore, when assessing your own retirement income needs, it might be wise not to depend solely on a pension.

1, 3) TIME.com, September 26, 2012

2) Yahoo! Finance, October 18, 2012

4) FoxBusiness.com, January 18, 2013

5) Milliman, 2013

6) The Wall Street Journal, September 21, 2012

7) The New York Times, July 20, 2012

INVESTING RISK DISCLOSURE

Keep in mind that investing involves risk. The value of your investment will fluctuate over time and you may gain or lose money. Before investing, consider the funds’ investment objectives, risks, charges, and expenses. Contact Mahoney Asset Management for a prospectus or, if available, a summary prospectus containing this information. Read it carefully.

IMPORTANT CONSUMER INFORMATION

This web site has been prepared solely for informational purposes. It is not an offer to buy or sell any security; nor is it a solicitation of an offer to buy or sell any security.This site and the opinions and information therein are based on sources which we believe to be dependable, but we can not guarantee the accuracy of such information.

Representatives of a broker-dealer or investment adviser may only conduct business in a state if the representatives and the broker-dealer or investment adviser they represent: (a) satisfy the qualification requirements of, and are approved to do business by, the state; or (b) are excluded or exempted from the state’s licenser requirements.

An investor may obtain information concerning a broker-dealer, an investment advisor, or a representative of a broker-dealer or an investment advisor, including their licenser status and disciplinary history, by contacting the investor’s state securities law administrator.

The financial calculator results shown represent analysis and estimates based on the assumptions you have provided, but they do not reflect all relevant elements of your personal situation. The actual effects of your financial decisions may vary significantly from these estimates–so these estimates should not be regarded as predictions, advice, or recommendations. Mahoney Asset Managment does not provide legal or tax advice. Be sure to consult with your own tax and legal advisors before taking any action that would have tax consequences.

SECURITIES: ARE NOT FDIC-INSURED/ARE NOT BANK-GUARANTEED/MAY LOSE VALUE

This information is intended for use only by residents of CA, CT, DC, FL,, MA, MD, MN, NC, NJ, NY, OH, PA, and VA. Ken Mahoney may only conduct securities business with residents of the states and/or jurisdiction for which they are properly registered.

Securities offered through Newbridge Securities Corporation, member FINRA, SIPC.

Investment Advisory services through NFSG Corporation an SEC Registered Investment Advisor.

Office of Supervisory Jurisdiction: 1200 N. Federal Hwy., Ste. 400, Boca Raton, FL 33432. Phone 954.334.3450 Fax 954.489.2390

Specific recommendations can only be based on review of a number of suitability factors including but not limited to the investors financial profile, investment objectives, risk tolerance and the investors review of appropriate offering documents. Past performance is no guarantee of future results. To help you make informed decisions, we provide you with essential disclosures, such as Regulation Best Interest (Reg BI), the Client Relationship Summary (CRS), and Form ADV. Linked sites are strictly provided as a courtesy. Newbridge Securities, Inc. does not guarantee, approve nor endorse the information or products available at the sites, nor do links indicate any association with or endorsement of the linked sites by Newbridge Securities.