Many people purchase term life insurance to help protect their families when their children are young and dependent on them for support. By definition, term policies have ending dates, and it’s not unusual to allow a term policy to lapse without obtaining replacement coverage after children leave home and can support themselves.

Even if you do not need life insurance to replace lost income for your dependents, you may want insurance for other purposes, such as paying final expenses or leaving a legacy. For these needs, you might consider a survivorship life insurance policy.

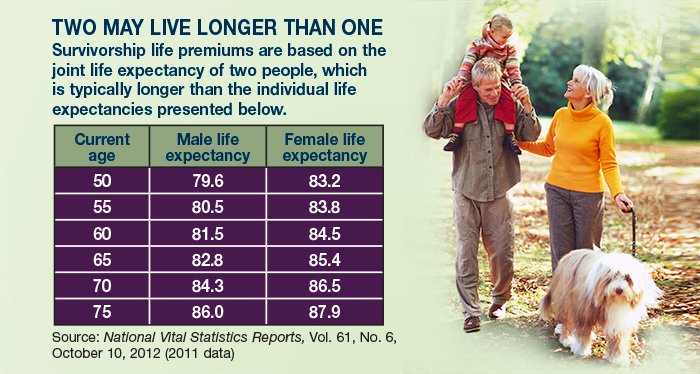

A Cost-Effective Approach

Also called second-to-die insurance, a survivorship life insurance policy insures two people and pays a benefit after the death of the second insured person. The premiums are usually less expensive than premiums for a single-life policy because they are based on the life expectancies of both insured individuals. This can be especially helpful later in life, when an individual life insurance policy may be more expensive or difficult to obtain. Survivorship policies can also be used to insure business partners, and options may be available to insure more than two people, if appropriate.

Survivorship life insurance is often used to pay estate taxes, which typically do not become an issue until estate assets pass to nonspouse heirs. Fewer estates may be subject to federal estate taxes now that the higher exemption amount ($5.25 million in 2013) has been made permanent by the American Taxpayer Relief Act of 2012. However, heirs often face other expenses in settling an estate, including probate and state estate taxes, which typically have lower exemption levels than federal estate taxes. The death benefit from a survivorship life insurance policy can help pay these expenses without requiring heirs to sell assets or dip into their inheritances.

As with most financial decisions, there are expenses associated with the purchase of life insurance. Policies commonly have mortality and expense charges. In addition, if a policy is surrendered prematurely, there may be surrender charges and income tax implications. The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Before implementing a strategy involving life insurance, it would be prudent to make sure that you are insurable.

INVESTING RISK DISCLOSURE

Keep in mind that investing involves risk. The value of your investment will fluctuate over time and you may gain or lose money. Before investing, consider the funds’ investment objectives, risks, charges, and expenses. Contact Mahoney Asset Management for a prospectus or, if available, a summary prospectus containing this information. Read it carefully.

IMPORTANT CONSUMER INFORMATION

This web site has been prepared solely for informational purposes. It is not an offer to buy or sell any security; nor is it a solicitation of an offer to buy or sell any security.This site and the opinions and information therein are based on sources which we believe to be dependable, but we can not guarantee the accuracy of such information.

Representatives of a broker-dealer or investment adviser may only conduct business in a state if the representatives and the broker-dealer or investment adviser they represent: (a) satisfy the qualification requirements of, and are approved to do business by, the state; or (b) are excluded or exempted from the state’s licenser requirements.

An investor may obtain information concerning a broker-dealer, an investment advisor, or a representative of a broker-dealer or an investment advisor, including their licenser status and disciplinary history, by contacting the investor’s state securities law administrator.

The financial calculator results shown represent analysis and estimates based on the assumptions you have provided, but they do not reflect all relevant elements of your personal situation. The actual effects of your financial decisions may vary significantly from these estimates–so these estimates should not be regarded as predictions, advice, or recommendations. Mahoney Asset Managment does not provide legal or tax advice. Be sure to consult with your own tax and legal advisors before taking any action that would have tax consequences.

SECURITIES: ARE NOT FDIC-INSURED/ARE NOT BANK-GUARANTEED/MAY LOSE VALUE

This information is intended for use only by residents of CA, CT, DC, FL,, MA, MD, MN, NC, NJ, NY, OH, PA, and VA. Ken Mahoney may only conduct securities business with residents of the states and/or jurisdiction for which they are properly registered.

Securities offered through Newbridge Securities Corporation, member FINRA, SIPC.

Investment Advisory services through NFSG Corporation an SEC Registered Investment Advisor.

Office of Supervisory Jurisdiction: 1200 N. Federal Hwy., Ste. 400, Boca Raton, FL 33432. Phone 954.334.3450 Fax 954.489.2390

Specific recommendations can only be based on review of a number of suitability factors including but not limited to the investors financial profile, investment objectives, risk tolerance and the investors review of appropriate offering documents. Past performance is no guarantee of future results. To help you make informed decisions, we provide you with essential disclosures, such as Regulation Best Interest (Reg BI), the Client Relationship Summary (CRS), and Form ADV. Linked sites are strictly provided as a courtesy. Newbridge Securities, Inc. does not guarantee, approve nor endorse the information or products available at the sites, nor do links indicate any association with or endorsement of the linked sites by Newbridge Securities.