According to a 2013 survey, almost 90% of middle-income Americans do not feel prepared to handle the financial cost of a critical illness. Most respondents said they would have to use their savings, but 75% had less than $20,000 in savings and 25% had no savings at all.1

A critical illness can be especially challenging, but even healthy people with medical insurance can face substantial out-of-pocket expenses. The total health-care cost for a typical family of four covered by an employer-sponsored PPO insurance plan is $22,030 in 2013. More than 40% of this total — $9,144 — is paid by employees through payroll deductions and out-of-pocket expenditures.2

One strategy that may help reduce health-care costs while saving for future expenses is to combine a high-deductible health plan (HDHP) with a health savings account (HSA).

Trade-Off for Lower Premiums

Individuals covered by an HDHP pay a relatively high annual deductible — at least $1,250 ($2,500 for families) in 2013 and 2014 — for services such as hospital care, physician visits, and prescriptions before the plan begins to pay a percentage of expenses. The costs for medical services may be reduced through the insurer’s negotiated rate, and certain types of preventive care, such as annual physicals and health screenings, may be provided at no cost. Some plans have higher deductibles.

The trade-off for potentially higher up-front expenses is that premiums are typically lower for HDHPs than they are for traditional PPO and HMO plans. To protect consumers from “catastrophic expenses,” HDHPs (and most other policies) are required to have out-of-pocket maximums above which the insurer pays all medical expenses.

Tax-Advantaged Savings

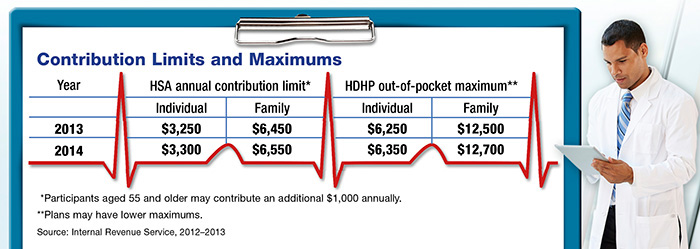

Only individuals who are enrolled in an HDHP are eligible to establish and contribute to an HSA, which is a tax-advantaged savings account that can be used to pay future medical expenses. HSA contributions are typically made through payroll deductions, but in most cases they can also be made directly to the HSA provider. (See the chart above for contribution limits.)

HSA funds can be withdrawn free of federal income tax and penalties as long as the money is spent on qualified health-care expenses. Depending on the state, HSA contributions and earnings may or may not be subject to state taxes.

Assets in an HSA belong to the contributor, so they can be retained in the account (typically with an investment option) even after the individual changes employers or retires. Unspent HSA balances can be used to help meet medical needs in future years, whether the account owner is enrolled in an HDHP or not. Although HSA funds cannot be used to pay regular health insurance premiums, they can be used to help pay Medicare premiums and long-term-care expenses.

The HDHP/HSA strategy is designed to help keep total medical costs down by encouraging consumers to focus on wellness, compare costs, and use in-network providers and generic prescription medicines. Although this requires some effort — and may not be appropriate for everyone — it could help you control your annual out-of-pocket expenses.

1) AdvisorOne, May 8, 2013

2) Milliman, 2013

INVESTING RISK DISCLOSURE

Keep in mind that investing involves risk. The value of your investment will fluctuate over time and you may gain or lose money. Before investing, consider the funds’ investment objectives, risks, charges, and expenses. Contact Mahoney Asset Management for a prospectus or, if available, a summary prospectus containing this information. Read it carefully.

IMPORTANT CONSUMER INFORMATION

This web site has been prepared solely for informational purposes. It is not an offer to buy or sell any security; nor is it a solicitation of an offer to buy or sell any security.This site and the opinions and information therein are based on sources which we believe to be dependable, but we can not guarantee the accuracy of such information.

Representatives of a broker-dealer or investment adviser may only conduct business in a state if the representatives and the broker-dealer or investment adviser they represent: (a) satisfy the qualification requirements of, and are approved to do business by, the state; or (b) are excluded or exempted from the state’s licenser requirements.

An investor may obtain information concerning a broker-dealer, an investment advisor, or a representative of a broker-dealer or an investment advisor, including their licenser status and disciplinary history, by contacting the investor’s state securities law administrator.

The financial calculator results shown represent analysis and estimates based on the assumptions you have provided, but they do not reflect all relevant elements of your personal situation. The actual effects of your financial decisions may vary significantly from these estimates–so these estimates should not be regarded as predictions, advice, or recommendations. Mahoney Asset Managment does not provide legal or tax advice. Be sure to consult with your own tax and legal advisors before taking any action that would have tax consequences.

SECURITIES: ARE NOT FDIC-INSURED/ARE NOT BANK-GUARANTEED/MAY LOSE VALUE

This information is intended for use only by residents of CA, CT, DC, FL,, MA, MD, MN, NC, NJ, NY, OH, PA, and VA. Ken Mahoney may only conduct securities business with residents of the states and/or jurisdiction for which they are properly registered.

Securities offered through Newbridge Securities Corporation, member FINRA, SIPC.

Investment Advisory services through NFSG Corporation an SEC Registered Investment Advisor.

Office of Supervisory Jurisdiction: 1200 N. Federal Hwy., Ste. 400, Boca Raton, FL 33432. Phone 954.334.3450 Fax 954.489.2390

Specific recommendations can only be based on review of a number of suitability factors including but not limited to the investors financial profile, investment objectives, risk tolerance and the investors review of appropriate offering documents. Past performance is no guarantee of future results. To help you make informed decisions, we provide you with essential disclosures, such as Regulation Best Interest (Reg BI), the Client Relationship Summary (CRS), and Form ADV. Linked sites are strictly provided as a courtesy. Newbridge Securities, Inc. does not guarantee, approve nor endorse the information or products available at the sites, nor do links indicate any association with or endorsement of the linked sites by Newbridge Securities.