Within certain guidelines, employers are generally allowed to auto-enroll workers in employer-sponsored retirement plans and divert a set percentage of compensation into workers’ accounts unless they specifically opt out or change the contribution rate. Automatic enrollment tends to boost participation; in fact, average participation for company plans with auto enrollment exceeds 85%, compared with 67% for plans without it.1

Thus, auto enrollment could make it more likely that a plan will pass the IRS nondiscrimination testing ordinarily required for traditional 401(k) plans. Auto enrollment can be added to any new or existing plan that allows elective salary deferrals, including 401(k)s and SIMPLE IRAs utilized by small businesses.

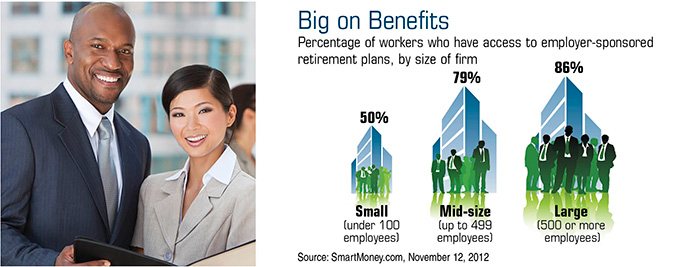

Comparing the benefits and limitations of various retirement plans may help you determine whether one of them might meet your company’s needs.

Safe Harbor 401(k) Plan

“Safe harbor” plans designed for smaller firms are typically more flexible than traditional 401(k)s offered by many large companies. Owners may be able to make larger contributions for themselves (as employee and employer) in exchange for making tax-deductible contributions or “matches” for employees.

The maximum employee contribution in 2013 and 2014 is $17,500 ($23,000 for those 50 and older). Employers must either match employee contributions — 100% of the first 3% of deferred salary plus 50% of the next 2% of deferred salary — or make a non-elective contribution of 3% of salary for each eligible employee. Match, profit share, and/or total contributions cannot exceed 100% of an employee’s compensation or $52,000 in 2014.

SIMPLE IRA

Companies with 100 or fewer employees may use a SIMPLE IRA salary-reduction plan, which requires little or no paperwork, if they do not currently have another retirement plan in place. The maximum employee contribution in 2013 and 2014 is $12,000 ($14,500 for those aged 50 and older). The required match is 100% of the first 3% of participant contributions or 2% of all eligible employee salaries.

Employer-sponsored retirement plan distributions are taxed as ordinary income. Withdrawals prior to age 59½ may be subject to a 10% federal income tax penalty. Early withdrawals (prior to age 59½) from a SIMPLE IRA during the first two years of participation may be subject to a 25% penalty (10% thereafter).

1) MarketWatch, March 15, 2013

INVESTING RISK DISCLOSURE

Keep in mind that investing involves risk. The value of your investment will fluctuate over time and you may gain or lose money. Before investing, consider the funds’ investment objectives, risks, charges, and expenses. Contact Mahoney Asset Management for a prospectus or, if available, a summary prospectus containing this information. Read it carefully.

IMPORTANT CONSUMER INFORMATION

This web site has been prepared solely for informational purposes. It is not an offer to buy or sell any security; nor is it a solicitation of an offer to buy or sell any security.This site and the opinions and information therein are based on sources which we believe to be dependable, but we can not guarantee the accuracy of such information.

Representatives of a broker-dealer or investment adviser may only conduct business in a state if the representatives and the broker-dealer or investment adviser they represent: (a) satisfy the qualification requirements of, and are approved to do business by, the state; or (b) are excluded or exempted from the state’s licenser requirements.

An investor may obtain information concerning a broker-dealer, an investment advisor, or a representative of a broker-dealer or an investment advisor, including their licenser status and disciplinary history, by contacting the investor’s state securities law administrator.

The financial calculator results shown represent analysis and estimates based on the assumptions you have provided, but they do not reflect all relevant elements of your personal situation. The actual effects of your financial decisions may vary significantly from these estimates–so these estimates should not be regarded as predictions, advice, or recommendations. Mahoney Asset Managment does not provide legal or tax advice. Be sure to consult with your own tax and legal advisors before taking any action that would have tax consequences.

SECURITIES: ARE NOT FDIC-INSURED/ARE NOT BANK-GUARANTEED/MAY LOSE VALUE

This information is intended for use only by residents of CA, CT, DC, FL,, MA, MD, MN, NC, NJ, NY, OH, PA, and VA. Ken Mahoney may only conduct securities business with residents of the states and/or jurisdiction for which they are properly registered.

Securities offered through Newbridge Securities Corporation, member FINRA, SIPC.

Investment Advisory services through NFSG Corporation an SEC Registered Investment Advisor.

Office of Supervisory Jurisdiction: 1200 N. Federal Hwy., Ste. 400, Boca Raton, FL 33432. Phone 954.334.3450 Fax 954.489.2390

Specific recommendations can only be based on review of a number of suitability factors including but not limited to the investors financial profile, investment objectives, risk tolerance and the investors review of appropriate offering documents. Past performance is no guarantee of future results. To help you make informed decisions, we provide you with essential disclosures, such as Regulation Best Interest (Reg BI), the Client Relationship Summary (CRS), and Form ADV. Linked sites are strictly provided as a courtesy. Newbridge Securities, Inc. does not guarantee, approve nor endorse the information or products available at the sites, nor do links indicate any association with or endorsement of the linked sites by Newbridge Securities.