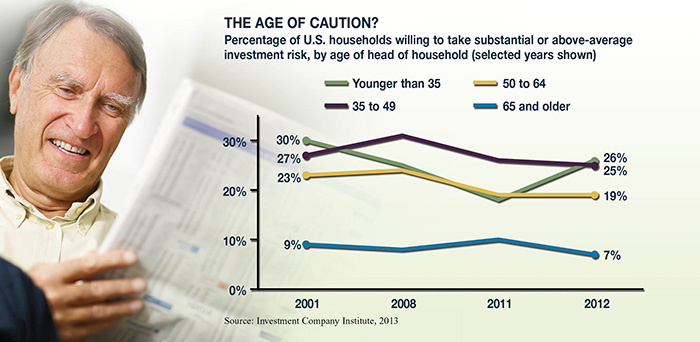

A recent academic study confirmed that willingness to take investment risk is affected not only by an investor’s age but by the current economic climate.1 The more conservative risk tolerance associated with age might be considered rational behavior, because older investors may have less time to recover from potential losses and generally need to tap their savings sooner than younger investors.

Changing one’s risk tolerance based on current economic conditions, however, may be less rational. Assuming more risk when the market is up and less risk when the market is down might encourage you to buy when prices are high and sell when prices are low.

Because no one can predict the market’s ups and downs, a wiser approach might be to adopt an investment strategy appropriate for your personal situation and to maintain it regardless of market volatility. Doing so could help you become a more rational investor.

Reference Points and Mental Accounts

The field of behavioral finance seeks to understand how and why investors react to different events and outcomes. It’s been widely accepted for some time that investors tend to react more negatively to losses than they react positively to gains. Recent research suggests that people have a subjective reference point for considering whether an investment is a success or a failure, and they may have different reference points for different investments. Investors also use mental accounts to organize investments for specific goals.2

Understanding your own reference points and mental accounts may help you determine an appropriate asset allocation based on your risk tolerance. Although asset allocation is a method to help manage investment risk, it does not guarantee against investment loss.

Hard-Wired Responses

Neuroscientists are discovering that many emotions and behaviors are “hard-wired” in the brain. In an experiment where investing was rewarded more highly than not investing, people with damage to areas of the brain related to emotions and risk — including the amygdala, orbitofrontal cortex, and insula regions — were not constrained by investment losses and achieved higher returns than those with healthy brains. In other studies, however, people with damage to these areas have gone “bankrupt” due to poor judgment and taking on too much risk.3

Another experiment, which looked at how people use past rewards to predict future payoffs, found that most subjects were unduly influenced by the two most recent results, perceiving a pattern where there was none. However, people with damage to a region of the brain called the frontopolar cortex made decisions primarily on cumulative reward history rather than on the most recent outcomes.4

The brain may also have a “motivation center” that drives efforts to achieve a goal based on the perceived value of success. In a series of tests, an increase in the dollar value of a potential reward created increased activity in a region of the brain called the ventral striatum, which led to increased efforts to achieve the reward.5

These findings suggest that investors may have to control natural responses that could lead to their becoming too risk averse, reacting too quickly, or pursuing potential gains without appropriate caution. If you become overly emotional when it comes to your investments, it may help to take a step back and consider the situation rationally based on your overall financial strategy.

1) University of Missouri, 2012

2) AdvisorOne.com, February 23, 2012

3) Forbes.com, October 16, 2012

4) The Wall Street Journal, July 21, 2012

5) ScienceDaily.com, February 22, 2012

INVESTING RISK DISCLOSURE

Keep in mind that investing involves risk. The value of your investment will fluctuate over time and you may gain or lose money. Before investing, consider the funds’ investment objectives, risks, charges, and expenses. Contact Mahoney Asset Management for a prospectus or, if available, a summary prospectus containing this information. Read it carefully.

IMPORTANT CONSUMER INFORMATION

This web site has been prepared solely for informational purposes. It is not an offer to buy or sell any security; nor is it a solicitation of an offer to buy or sell any security.This site and the opinions and information therein are based on sources which we believe to be dependable, but we can not guarantee the accuracy of such information.

Representatives of a broker-dealer or investment adviser may only conduct business in a state if the representatives and the broker-dealer or investment adviser they represent: (a) satisfy the qualification requirements of, and are approved to do business by, the state; or (b) are excluded or exempted from the state’s licenser requirements.

An investor may obtain information concerning a broker-dealer, an investment advisor, or a representative of a broker-dealer or an investment advisor, including their licenser status and disciplinary history, by contacting the investor’s state securities law administrator.

The financial calculator results shown represent analysis and estimates based on the assumptions you have provided, but they do not reflect all relevant elements of your personal situation. The actual effects of your financial decisions may vary significantly from these estimates–so these estimates should not be regarded as predictions, advice, or recommendations. Mahoney Asset Managment does not provide legal or tax advice. Be sure to consult with your own tax and legal advisors before taking any action that would have tax consequences.

SECURITIES: ARE NOT FDIC-INSURED/ARE NOT BANK-GUARANTEED/MAY LOSE VALUE

This information is intended for use only by residents of CA, CT, DC, FL,, MA, MD, MN, NC, NJ, NY, OH, PA, and VA. Ken Mahoney may only conduct securities business with residents of the states and/or jurisdiction for which they are properly registered.

Securities offered through Newbridge Securities Corporation, member FINRA, SIPC.

Investment Advisory services through NFSG Corporation an SEC Registered Investment Advisor.

Office of Supervisory Jurisdiction: 1200 N. Federal Hwy., Ste. 400, Boca Raton, FL 33432. Phone 954.334.3450 Fax 954.489.2390

Specific recommendations can only be based on review of a number of suitability factors including but not limited to the investors financial profile, investment objectives, risk tolerance and the investors review of appropriate offering documents. Past performance is no guarantee of future results. To help you make informed decisions, we provide you with essential disclosures, such as Regulation Best Interest (Reg BI), the Client Relationship Summary (CRS), and Form ADV. Linked sites are strictly provided as a courtesy. Newbridge Securities, Inc. does not guarantee, approve nor endorse the information or products available at the sites, nor do links indicate any association with or endorsement of the linked sites by Newbridge Securities.