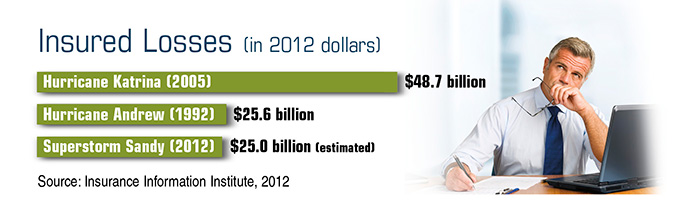

Superstorm Sandy wreaked havoc along the East Coast in 2012, leaving behind an estimated $50 billion to $60 billion in insured and uninsured economic losses. It’s likely that more than 150,000 insurance claims were ultimately paid to business owners.¹

Small businesses often operate on tight margins, so they can be hit especially hard when extreme weather or a more isolated event results in damage and/or forces a temporary closure. Unfortunately, one-fourth of small businesses never reopen after a major disaster.² Companies with a thoughtful disaster plan and adequate insurance protection may be in a better position to avoid such a fate.

Crafting Coverage

A business owner policy (BOP) is a package that typically includes insurance (up to policy limits) for property damage, liability, and business interruption. Property insurance helps protect a company’s buildings and equipment against a specific list of perils, similar to the coverage offered in a standard homeowners policy.

Business interruption insurance covers lost profits and operating expenses that may continue while a business is closed because of a disaster. There is generally a 48- or 72-hour waiting period before coverage begins.

This type of insurance may apply only if there is physical damage to the structure or the property is inaccessible because of an Order of Civil Authority (and only if the order resulted from a covered peril). Consequently, a business that is shut down due to a power outage may not be covered unless an optional endorsement for “off-premises service interruption” is purchased at an additional cost.

Floods are usually excluded from BOPs, but coverage may be available from the government’s National Flood Insurance Program or some private insurers. Unfortunately, only about 20% of the businesses affected by Sandy had flood insurance.³ Earthquakes are also typically excluded from BOPs.

Poised to Recover

When forming your disaster plan, schedule annual insurance reviews to make sure your coverage is keeping up with company changes. Updating your policy is especially important if you have expanded or purchased new equipment. Try to keep an accurate business inventory and take photos of the premises and all your business property.

Store these and other financial records online so they can be accessed from a temporary location, if needed. Good documentation may speed up the claims process and help you reopen for business as soon as possible.

1, 3) Insurance Information Institute, 2012

2) The Wall Street Journal, October 21, 2012

INVESTING RISK DISCLOSURE

Keep in mind that investing involves risk. The value of your investment will fluctuate over time and you may gain or lose money. Before investing, consider the funds’ investment objectives, risks, charges, and expenses. Contact Mahoney Asset Management for a prospectus or, if available, a summary prospectus containing this information. Read it carefully.

IMPORTANT CONSUMER INFORMATION

This web site has been prepared solely for informational purposes. It is not an offer to buy or sell any security; nor is it a solicitation of an offer to buy or sell any security.This site and the opinions and information therein are based on sources which we believe to be dependable, but we can not guarantee the accuracy of such information.

Representatives of a broker-dealer or investment adviser may only conduct business in a state if the representatives and the broker-dealer or investment adviser they represent: (a) satisfy the qualification requirements of, and are approved to do business by, the state; or (b) are excluded or exempted from the state’s licenser requirements.

An investor may obtain information concerning a broker-dealer, an investment advisor, or a representative of a broker-dealer or an investment advisor, including their licenser status and disciplinary history, by contacting the investor’s state securities law administrator.

The financial calculator results shown represent analysis and estimates based on the assumptions you have provided, but they do not reflect all relevant elements of your personal situation. The actual effects of your financial decisions may vary significantly from these estimates–so these estimates should not be regarded as predictions, advice, or recommendations. Mahoney Asset Managment does not provide legal or tax advice. Be sure to consult with your own tax and legal advisors before taking any action that would have tax consequences.

SECURITIES: ARE NOT FDIC-INSURED/ARE NOT BANK-GUARANTEED/MAY LOSE VALUE

This information is intended for use only by residents of CA, CT, DC, FL,, MA, MD, MN, NC, NJ, NY, OH, PA, and VA. Ken Mahoney may only conduct securities business with residents of the states and/or jurisdiction for which they are properly registered.

Securities offered through Newbridge Securities Corporation, member FINRA, SIPC.

Investment Advisory services through NFSG Corporation an SEC Registered Investment Advisor.

Office of Supervisory Jurisdiction: 1200 N. Federal Hwy., Ste. 400, Boca Raton, FL 33432. Phone 954.334.3450 Fax 954.489.2390

Specific recommendations can only be based on review of a number of suitability factors including but not limited to the investors financial profile, investment objectives, risk tolerance and the investors review of appropriate offering documents. Past performance is no guarantee of future results. To help you make informed decisions, we provide you with essential disclosures, such as Regulation Best Interest (Reg BI), the Client Relationship Summary (CRS), and Form ADV. Linked sites are strictly provided as a courtesy. Newbridge Securities, Inc. does not guarantee, approve nor endorse the information or products available at the sites, nor do links indicate any association with or endorsement of the linked sites by Newbridge Securities.