There’s plenty of guidance available to help you feel confident that it’s time to retire. But it could be just as important to recognize signs that you may not be ready. You might think of these as yellow caution lights, warning you to slow down and give further thought to your situation.

You’ve reached the eligibility age for Social Security

For some people, Social Security eligibility is synonymous with retirement. In fact, about 50% of those who are eligible for benefits file at the earliest age of 62, despite the fact that their monthly payments will be permanently reduced.¹

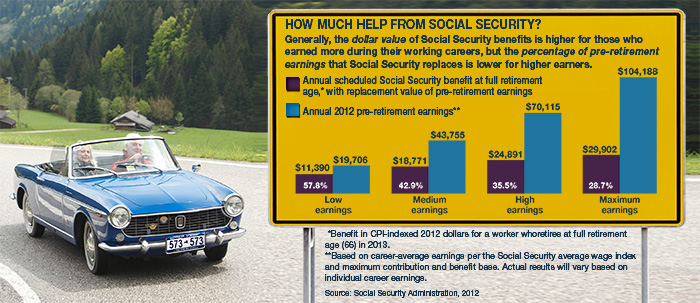

Even if you have reached full retirement age (age 66 for those born between 1943 and 1954), you may not be ready to retire unless you expect to receive substantial income from savings and/or other sources. Social Security is intended to replace only a portion of your pre-retirement income (see chart). Benefits increase at filing ages up to 70.

You need to work part-time

Sixty-five percent of older workers say they would like to continue working in some capacity during retirement.² That’s a worthwhile goal if you can do it by choice, but be careful if you expect to depend on part-time income. Jobs are not easy to find, and many part-time positions pay low wages. It might be wise to work in your current job a little longer to help build additional savings.

You’re counting on market growth

The rapid decline in stock values during the Great Recession and slow growth during the recovery suggest that it might not be wise to factor high returns into your retirement strategy. In fact, when you retire or are close to retirement, you may want to shift more of your assets to conservative investments. Doing so could help preserve principal but typically is associated with lower growth potential.

You’re not prepared for medical costs

In a recent poll, the high cost of medical care was retirees’ biggest surprise regarding retirement expenses.³ Even with current Medicare benefits, it’s estimated that a couple who retired in 2012 at age 65 would need $240,000 to pay their out-of-pocket medical expenses in retirement.4

Your spouse is not on board with your decision to retire

About three out of five married couples disagree on the timing of their retirements.5 Whether you decide to retire together or several years apart, it’s important for you and your spouse to be comfortable with the other’s choice to retire or continue working.

You have high debt or other financial obligations

Traditional formulas for determining retirement income needs often assume that retirees have paid off their mortgages. If you are still making payments on your home, have college loans or high credit-card debt, or are supporting your children or aging parents, you may not be ready to leave the workforce.

The road to retirement can have many twists and turns. A yellow light may be a timely warning that you are not quite ready to go full speed ahead.

1) SmartMoney.com, March 2, 2012

2) usnews.com, February 10, 2012

3) PRNewswire, July 11, 2012

4) NYTimes.com, May 9, 2012

5) WSJ.com, April 9, 2012

INVESTING RISK DISCLOSURE

Keep in mind that investing involves risk. The value of your investment will fluctuate over time and you may gain or lose money. Before investing, consider the funds’ investment objectives, risks, charges, and expenses. Contact Mahoney Asset Management for a prospectus or, if available, a summary prospectus containing this information. Read it carefully.

IMPORTANT CONSUMER INFORMATION

This web site has been prepared solely for informational purposes. It is not an offer to buy or sell any security; nor is it a solicitation of an offer to buy or sell any security.This site and the opinions and information therein are based on sources which we believe to be dependable, but we can not guarantee the accuracy of such information.

Representatives of a broker-dealer or investment adviser may only conduct business in a state if the representatives and the broker-dealer or investment adviser they represent: (a) satisfy the qualification requirements of, and are approved to do business by, the state; or (b) are excluded or exempted from the state’s licenser requirements.

An investor may obtain information concerning a broker-dealer, an investment advisor, or a representative of a broker-dealer or an investment advisor, including their licenser status and disciplinary history, by contacting the investor’s state securities law administrator.

The financial calculator results shown represent analysis and estimates based on the assumptions you have provided, but they do not reflect all relevant elements of your personal situation. The actual effects of your financial decisions may vary significantly from these estimates–so these estimates should not be regarded as predictions, advice, or recommendations. Mahoney Asset Managment does not provide legal or tax advice. Be sure to consult with your own tax and legal advisors before taking any action that would have tax consequences.

SECURITIES: ARE NOT FDIC-INSURED/ARE NOT BANK-GUARANTEED/MAY LOSE VALUE

This information is intended for use only by residents of CA, CT, DC, FL,, MA, MD, MN, NC, NJ, NY, OH, PA, and VA. Ken Mahoney may only conduct securities business with residents of the states and/or jurisdiction for which they are properly registered.

Securities offered through Newbridge Securities Corporation, member FINRA, SIPC.

Investment Advisory services through NFSG Corporation an SEC Registered Investment Advisor.

Office of Supervisory Jurisdiction: 1200 N. Federal Hwy., Ste. 400, Boca Raton, FL 33432. Phone 954.334.3450 Fax 954.489.2390

Specific recommendations can only be based on review of a number of suitability factors including but not limited to the investors financial profile, investment objectives, risk tolerance and the investors review of appropriate offering documents. Past performance is no guarantee of future results. To help you make informed decisions, we provide you with essential disclosures, such as Regulation Best Interest (Reg BI), the Client Relationship Summary (CRS), and Form ADV. Linked sites are strictly provided as a courtesy. Newbridge Securities, Inc. does not guarantee, approve nor endorse the information or products available at the sites, nor do links indicate any association with or endorsement of the linked sites by Newbridge Securities.